How To Be A Super Saver

A super saver is a person who saves a lot of money. On the average they save 15% or more of their income for retirement, but retirement isn’t the only thing they save for. They have a savings plan for anything that requires a cash outlay. Super savers have discovered ways to save more money than most Americans. If you want to know how to be a super saver, read on.

There are many benefits of being a super saver.

Did you know that the average American doesn’t have $400 in cash that they can lay their hands on? That’s right…most Americans don’t have enough money saved to handle a $400 emergency with cash. (Note: Not many years ago, this was said about an emergency of $1,000. That should tell you that, in general, we’re not getting any better about saving.)

You can be a super saver

Saving money is frugal: Being frugal is important. Because you can’t save money if you spend all of your money. I wrote an article “How I Save Money Being frugal”. This article explains why you need to be frugal in order to save money.

How To Become A Saver When You Are A Spender

You are what you do. Meaning if you save money you are a saver. If you spend all of your money. You are a spender.

It’s all about what you do. If you need help becoming a saver read this article for more information that will help you make the transition from being a spender to being a saver.

Mindset

To be a super saver, a person needs to commit to saving more money that the average American.

As Americans we tend to consume all we have. If you’re serious about being a super saver, you need to change from a mentality of “I receive and I consume” to an “I receive, I save, and I make do with what’s left over” mentality.

There is more to being a super saver than just trying to save more money. You need a lifestyle that supports your goal of saving more.

How To Be A Super Saver

You need a plan—actionable steps—that allows you to save more money than you do now. You need to be frugal.

Anyone Can Be A Super Saver

Before you can maximize a super saving plan, there are a couple of things you may need to do: become debt free and find a cheaper place to live—or get a roommate. Doing these two things will lower your cost of living. That should

Save money get a roommate or Earn money get a roommate

give you more money to save.

Note: Super saving requires you to live below your means.

I’m sure you can think of other ways to reduce your cost of living. Curtailing things like eating out, smoking, and getting rid of cable will increase the amount of money you have for saving.

Here’s another important step to take: Start building an emergency account. Having money to specifically handle emergencies can prevent the need to raid your super savings when something goes awry (and you know it will at some point).

Emergency Accounts

You need to have an emergency account to which you make regular contributions. A fund dedicated to dealing with emergencies on a cash basis protects the goal of being a super saver. It can also enhance your progress towards that goal; you’ll have money for emergencies and may be able to continue saving as you go through them.

Hint: An emergency account should be one of the categories in your budget. Contribute to your emergency account faithfully. That money can save you from a lot of grief when you need funds quickly.

How Much Do You Want To Put In Your Savings (Or Retirement) Account

Decide how much money you’re going to save. For planning purposes, it’s best to use a whole dollar amount based on a percentage. That way you can easily look at your savings or retirement plan and see how much you’ve contributed (or removed), and you can chart your progress.

Percentages

If you want to save 15% of your gross pay, multiply your pay by .15. That figure is the dollar amount you need to add to your long-term savings. (I usually round up to an even $5 amount: $143.50 becomes a deposit of $145 or $150.)

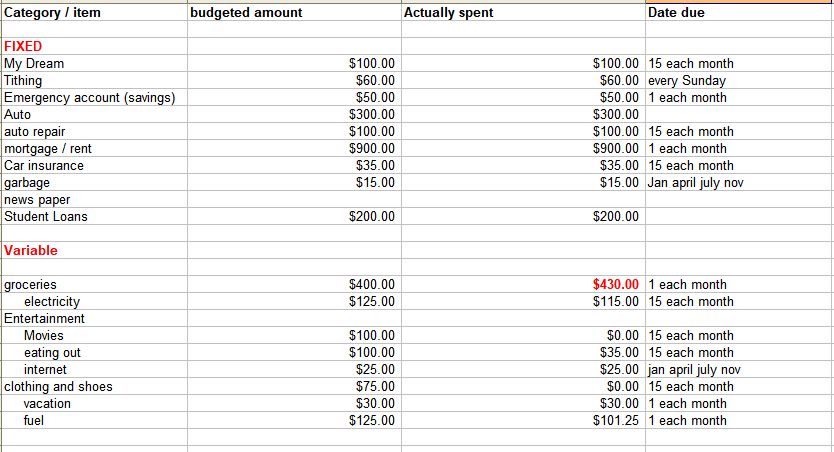

Budget

A good budget governs the amount(s) you allow for spending and how you spend. For the most part, its focus will

How to make a budget.

be on your funds for day to day living, but it should also include the not so ordinary things, things like the eventual need to replace your electronic devices or automobile, and your child’s college education. An important part of a good budget is Sinking funds.

(Note: The best budget in the world will not do you any good if you don’t live by it.)

Sinking Funds

Sinking funds provide a way to save for the expected and the unexpected before you need the money.

Sinking funds give you a place to set money aside for the usual and not so usual expenses like Christmas, a newer car, and upcoming bills. Every pay period you add a little money to the designated sinking fund. (Actually, you could add to all of them, but most of us have so many calls on our money that we need to have a scheduled cycle for the deposits.) Make your deposits until you have enough money to pay cash for the specified item or cause. If a sinking fund is fully funded you can use the money you were putting in it to increase your deposits to another sinking fund—until you spend and have to rebuild the original one.

By setting money aside in sinking funds every payday, you should be able to pay cash and avoid borrowing money. You won’t have to repay money you don’t really have, and you’ll save the money you would have spent in interest payments. This in turn makes you a little less dependent on your job and helps keep your cost of living down:

WIN + WIN = (A BIG)WIN

I recommend using sinking funds for everything that requires repair, replacement, or widely spaced payments—among others, an annual bus pass, tires for the car, and car insurance (if you pay it quarterly or semiannually).

The Thing Is

To be a successful super saver, you need to save money, pay cash for everything, and avoid debt.

Added Bonus

If you use sinking funds, you’ll have fewer incidents that are financial emergencies. You won’t need to raid your emergency account as often, because you’ll have a sinking fund for the small things that just happen (like fixing a flat tire) and things you know that are going to come eventually (like the need for a new set of tires). In other words you save for car repairs (or maintenance), and you have the funds to get the car taken care of when the need arises. You’ll pay for it from your sinking fund rather than from your emergency fund.

That practice applies to many facets of financial need other than just keeping your car on the road. (Think about all the gifts you buy and donations you make in the course of a year.) Also, knowing you have a plan to cover “life happens,” should make it easier to save for things—like retirement—that truly require a regular, long-term commitment.

Of course, within your plan there needs to be elements that help you stick to it…

Keep A Spending Journal

A spending journal is a record keeping practice that you update daily. Cash, credit, or debit card, it doesn’t matter. If you spend money, enter each outlay in your spending journal every day. I carry a small notebook with me and jot down pertinent information—how much, for what, and when—at the time that I spend the money or as soon as convenient (often when I get to the car). When I get home I update my spending journal. It keeps me current on

We all need a spending journal because we cant remember where all the money goes.

my spending habits.

Maintain Your Determination

Determination is more than just following a budget, more than going through the motions. It’s staying motivated, continually looking for ways to be more efficient: Make your money work better for you.

After you’ve decided you’re going to be a super saver, look for more ways to accomplish the task. As in any plan, you’ll encounter obstacles and opportunities to abandon your goal, but your determination can provide the drive to find ways to work around impediments. Try staying a step ahead of complications, read about or even better talk to people who are super savers. Tap them for ideas on “staying power” for when life isn’t going your way.

Of course, you’ll be determined to stay within your budget, but you need to be open-minded and willing to change your budget when necessary. Change isn’t always good, but it doesn’t necessarily have to be bad. To make a frugal decision about deviating from your budget, you need to ask yourself if an expenditure is likely to put you closer to reaching your goal. If the answer is “No,” you may not want to spend the money. Making decisions that move us toward our goals, regardless our feelings is an important factor of determination. As an example, let’s say you have the opportunity to make a new investment…or, maybe, you’re thinking about buying a second car. (The investment might be a good move. The car??? Well, probably not—if it’s only for fun or even convenience. However, if the car was to provide your spouse with the means to get to work and increase your opportunity to save, then maybe, it would be a profitable expenditure.)

Set Goals

Judging your progress is next to impossible if you don’t have goals. You need to have one major goal made up of many mini-goals (milestones). The mini-goals are—essentially—your plan for reaching the major goal. You can keep track of your progress towards the ultimate goal as you accomplish your plan.

To be worthwhile a goal needs to be specific, measurable, attainable, realistic, and timely. I wrote a post about setting SMART goals. Take time to read it.

Note: Watching our progress toward a major goal should be very rewarding, but with long-term goals many of us want something more concrete that reminds us that we’re doing a good job. As you meet mini goals, include an occasional reward for yourself. It could be anything, something like a modest “victory” dinner when you reach a designated point. Mine is to visit a barbershop a couple of times a year, but only if I’m on track with my savings. (My wife usually cuts my hair, so this can give us both a break.) Rewarding yourself is very powerful method for staying motivated.

Keep Needs And Wants In Perspective

This is really important: You have to know what you really need for living and to make progress towards your goal. You also need to be aware of your (unnecessary) “wants.” Make sure your lifestyle is not driven by them. Here’s an example: You might need a car to get to work, but you don’t nee a brand new car (no matter how much you may want one). A good used car will get you to work just as well as a new one. A good used car without payments is even better. (Keep your cost of living low.)

Work to keep your costs of living low. However, if you have a few reasonable “wants,” especially ones that would enhance your quality of living, both now and in the future, you might think about using them as those rewards I just talked about.

Bonus

Part-time Employment Or Side Hustle

As you quest to save more money, you may find it expedient to take on a part time job or side hustle that brings in more money. If you do pursue greater income, it’s important to remember why you are working: The reason should be that you can save more money. Make sure you save what you set out to save. (Increased income should allow you to increase the amount you save or decrease the amount of time it will take to meet the goal you’ve set. (Increased income should not be considered as a means to indulge it more “wants.”

Suggestions for side hustles

Selling blood plasma

Detailing cars

Yard work

House sitting

Of course, you can find a part-time job, but I want you to be aware that there are many ways to earn extra money being self-employed.

A second job can help you reach your goal.

Conclusion

Super savers save more money than the average American—usually with retirement in mind. In order to save that money, they must have a good budget and take decisive action to save. They have budgets that include categories and sinking funds for savings as well as an emergency account. They often work second jobs or side hustles to increase their income and save that money as well. You can be a super saver.