Why Frugal Living Works

Almost everyone is frugal to some extent. That’s because frugal living works. You take care of current need while preparing for the future.

Let’s say, every time you get paid, you set money aside for the next month’s rent or gas for your car, a dinner date, a special (expensive) cup of coffee, or something else that’s important to you, that’s frugal. By saving that way, it’s very likely you’ll have the funds to cover the purchase or event when it occurs. But… while saving this way is good, these are incidental frugal acts. They are not necessarily indicative of a frugal lifestyle. A frugal lifestyle doesn’t just fund a single favorite part of your life—or even a few. It requires the same consideration for the financial aspect of all its facets.

Why Frugal Living Works

Too often, people are caught up in the habit of living for the moment, a lifestyle that demands immediate gratification. Let’s be honest, we all should know we can’t have everything, and we certainly can’t have it all “right now”. We each can, however, determine what we need and really want out of life. We can make a plan—set goals—to achieve those things and take action to make them happen. Fugal living works because it’s a proactive lifestyle.

While I’m thinking about it, there’s something I’d like to note: When people talk about frugal living, it’s almost invariably about using money wisely, maximizing it’s potential. I tend to conform to that mold. But I’d be remiss if I didn’t say that a truly frugal lifestyle maximizes all your resources. Time and talent are two that can definitely contribute to your financial strength. Think about it, the sooner you adopt a frugal lifestyle the longer you have to increase your money’s means to produce more, and talent can enhance your earning (and, therefore, saving) potential. Money, currently available or as income potential, along with time and talent should always be considered when you think about why frugal living works better than some other lifestyles. That said, use the following basic practices to facilitate developing a frugal living plan.

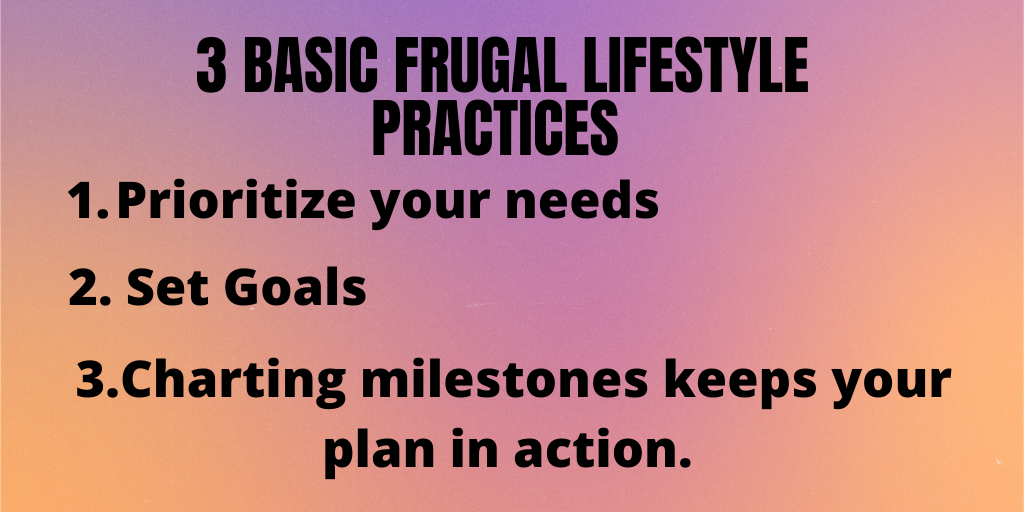

Three Basic Frugal Lifestyle Practices

-

Prioritize your needs

. Make a list of everything in your life that requires funds. Determine what is imperative for you to apply money towards. Put the things you need to cover regularly at the top of the list. These will be recurring expenses, including debt payments, along with savings for emergencies and retirement. Follow this with things that are likely to become important, the purchase, maintenance, or replacement of various items like houses, cars, computers, appliances, phones, clothes, education, vacations…

This list will be the basis for a budget. Using it you can allocate your income effectively. The list will be extensive. It should be as comprehensive as possible. And, since you’re frugal, you’ll revise it over time as you see ways to make your money work more efficiently.

-

Set goals

. Once you can see the things that present an immediate demand on your money, you can begin to put together a budget. The purpose of budgeting is to organize (save) your money so that when payments (and I’m not just talking about loan or credit payments, but expenditures in general) are required, you consistently have the funds to meet them. At a minimum the intent is to have a life of sufficient provision. Ultimately, of course, we all want more than that. To achieve this, many frugal people make time sensitive goals for saving the money required for each expense ahead of actually needing it. For each, they save, in increments, a set amount from every paycheck. The idea is to break the total amount of any—and every—expenditure into smaller pieces with the full amount saved by the time it’s needed. Take a look at my article on budgeting. It explains the process in detail.

-

Charting milestones keeps your plan in action.

A budget—your saving/spending plan—is a great tool, but you have to actually use for it to be effective. Go ahead and take the action needed to make your money work for you. As an incentive, especially for larger outlays, track your progress. If you’re paying down a loan or saving for something expensive, it’s gratifying to see when you’ve reached certain points—milestones of say, 10, 25, 50, 75, or 90 percent. (You pick the numbers.) On a calendar or spreadsheet, mark the dates when you should reach these significant points. Then, as you reach them, cross them off.

I’ve called these three hacks “practices” since you’ll repeat them as you take control of your finances and your ability to diversify the allocation of funds increases. Life is dynamic. Circumstances change. They can be accommodated. You’ll handle the accommodations through the enduring frugal lifestyle premise: Take care of today while preparing for the future. That’s a major reason why frugal living works.

Life: More Than Just Needs

When I wrote the section on prioritizing, I talked about making your money meet your immediate financial needs. I also included a list of things that things that might not be urgent to fund now but could become so in the future, like replacing a computer or more education. Some of those things, like more education (and yes, I know I’m repeating “education”) or a great vacation (Maybe zorbing in New Zealand???), might even seem like dreams. Regardless, funding for these is handled the same way as it is for current matters—incrementally.

But…you might say it’s a challenge to meet even the most basic of your present expenses, your current needs.

In that case, as a frugal person you, again, take action. Money isn’t your only resource. You have time and talent. Those assets can help increase your earning power (Think, side job) or make your earnings go further (Think, cut waste). A willingness to use of all your assets to enhance your earning power and the effectiveness of your spending is another reason why frugal living works. Also, you don’t have to fund everything instantly. As you earn more money, pay off debt, and cut waste, you can ease into saving for the less immediate needs—and for your dreams, your wants.

The amount of money you spend is largely up to you. Therefore, this is true:

The amount of money you don’t spend is also largely up to you. You can find ways to save. Frugal living works.

Addressing Need

The more you spend on your needs the less you have to put away for your dreams, your wants. The following is a list of ways (practices) can help you reduce what you spend on day to day living. By no means is it complete, but it gives you starting points for finding ways to save money.

Housing

We can elect to live in the most expensive place we can afford, or we can settle for a little less. We can even choose to settle for a lot less. You can save money by choosing to live below your means when it comes to housing. Another way to bring down your housing costs is to get a roommate, someone to share the expenses.

Utilities

Housing and utilities are usually connected. You can save money by doing something as simple as turning off the lights when you leave a room. Using a programable thermostat and keeping the room temperature just comfortable rather than excessively warm or cool can keep utility bills down. (I mean, isn’t it silly to set your air conditioner so low you need to wear a sweater indoors in the summer??? But…I bet each of us knows someone who does just that. That’s definitely not a frugal practice and increases what you spend on utilities.)

Fast Food, Fine Dining, and Home Cooking

Where do you eat most of your meals? Or maybe, it would be better to ask where you buy most of your food? I’ve seen TV programs reveal the kitchens of certain character types. In them, you see empty cupboards and only a box of cereal (always stale) on the counter and a bottle of wine or some beer in in the refrigerator. Usually, the character is male, and he’s either much too busy climbing the corporate ladder or a derelict. The implication is that those two types of people either don’t eat or eat every meal out. While most of us don’t cast ourselves in either of those two stereotypical roles, and our kitchens may hold the makings for several wonderful meals, we still eat out—a lot. We think picking up something at a drive-thru saves time and mess…

What do you think you’re paying for when you buy a beverage, a snack, or a meal, from a fast food place? For sure, the food. You, also, pay for their time and mess, plus more, and you don’t get it at their cost. They want to recoup and make a profit on the price they pay to operate their business. But… you have a refrigerator, cupboards, and a pantry full of much healthier stuff! (BTW: Like money, time, and talent, health is another of your assets and shouldn’t be wasted. It contributes to your ability to make money and to enjoy what your money can bring you.)

If you see how you’re paying an inflated price for food you buy at a drive-thru, I’m sure you can see how the logic carries over to full-service restaurants. Depending on the type of food, service, and ambience factors, we can call them fine dining establishments. (I’m saying this for clarification, not to be sarcastic. After all, I enjoy eating in a nice restaurant once in a while, too.) The essential difference between places that are sit-down verses those that are primarily drive-thru is that with the upgrades come increased prices. There is, however, one other factor to consider: If you don’t pull a Supersize Me, don’t ask for double meats or anything bigger than a medium for sides and beverages at a fast food place, your order is usually sufficient to serve one person. At a sit-down restaurant, standard issue is about enough for three people. When I go to a nice restaurant, I eat one third to one half of my meal and take the rest home. That gives me the basics for one to two more meals. (Just so you know, I like to eat at a good restaurant every few weeks. It’s part of my budget. Out of every paycheck, I set a few dollars aside to do so. That way a “sudden urge” to eat out doesn’t interfere with taking care of everyday expenses. (That’s an example of how budgeting works in a frugal lifestyle.)

I think it’s clear that if you eat every meal out, you’ll pay a lot more for food than if you eat at home. But there are also ways to reduce the cost of homecooked meals. Have a meal plan and use it to shop for food. When items you need are on sale, take advantage of the price break. Buy generic. Use coupons. Maybe, plant a garden. (You can use the produce fresh, or freeze, or can it.) Here’s something you may not have thought of: Cut down on how much you eat. Overeating is expensive. It’s really a form of waste. Part of the reason why frugal living works is because you’re on the lookout to cut waste.

Although many people waste a lot of money on food, you don’t have to. You may already use some of the moneysaving habits I mentioned above. That’s a good thing! Those practices fit with my earlier statement about most people being frugal to some extent.

Clothing

Do all your clothes need to be name brand and/or new? That usually means pricey. There’s a less expensive alternative—thrift stores. You might be surprised at the amount of quality clothing you can find at a thrift store, and prices are very reasonable. Reasonable prices mean you put less of your income towards something. That leaves more money to put towards other needs or dreams. That’s the object of frugal living.

Personal Transportation

When you make that list of important financial concerns (See above: Three Basic Frugal Lifestyle Practices), your car and associated issues will probably take several top spots. You have to maintain the vehicle, fuel it, insure it (Take a look at my article save money on your car insurance.) At some point, you’ll also need to replace it. Owning a car is expensive. Buying a new one is more so.

More than likely, you’ve gone through the new car buying experience. And, you took out a loan to pay for it. So, not only did you have to pay for the car, you had to pay interest—the price for using someone else’s money. How long did you have to make payments? I’m guessing several years, but it probably seemed like forever.

Living frugally and preparing ahead of time for the purchase of a new car can make the expense of buying one easier to afford. Saving for the purchase incrementally while you still have control of that money (and could apply it to something else if needed) keeps those funds at your disposal until the day you decide to put them to their intended use. If you sign loan papers, however, you sign away your right to use the amount of money due monthly (month after month, year after year) for any other purpose.

Saving to buy a new car is a frugal practice, saving to buy a good quality used car is even better.

Did you know new cars tend to depreciate in value about 47% over their first three years on the road? Most new car buyers can’t pay off their loans in that amount of time, but the price a 3-year old car that’s for sale by owner or in a used car lot should come close to reflecting that depreciation. If it’s in good shape and you can pay cash for it, you’ll have a good deal and a frugal lifestyle success.

I’m not going to go into all the ins and outs of buying a used car in this article. I’ve already done that. Read my post used car inspection checklist. It will show you what to look for. (BTW: Here’s bonus, auto insurance is usually much cheaper for used cars than new ones.)

Saved Money

Question: What do you do with money you “find” by cutting expenses?

Answer: Save it, of course.

You could use those savings to pay down debt. Eliminating debt leads yields money to use for something else. Or, you could start saving for something that, so far, has only been a dream, like retiring early or taking a cooking class—in France. If you have your needs covered and are satisfied with how your future looks, you can use your money as you choose. (Of course, becoming frugal was that same option. You chose to be frugal because you knew your money could do more than it’d been doing for you.)

Conclusion

I know I haven’t covered all the financial issues in anybody’s life, but think about the takeaways from the examples I’ve shown you. You can find ways to spend less. That gives you money to save more or to pay down debt.

Satisfying your basic needs doesn’t require “new” or “expensive”. Again, that leaves you with more money to work for you. You should reach a point where you’re putting away money for more than just current expenses. You need to find ways to prepare for your future. That includes making some dreams come true. Living frugally gives you a great opportunity to succeed in doing that.

Living frugally allows us to allocate our money for specific purposes and incrementally build funds for those purposes. It’s a lifetime lifestyle that addresses current and future financial issues. That means we can have the money we need when we need it. We can have financial security. That’s why frugal living works.